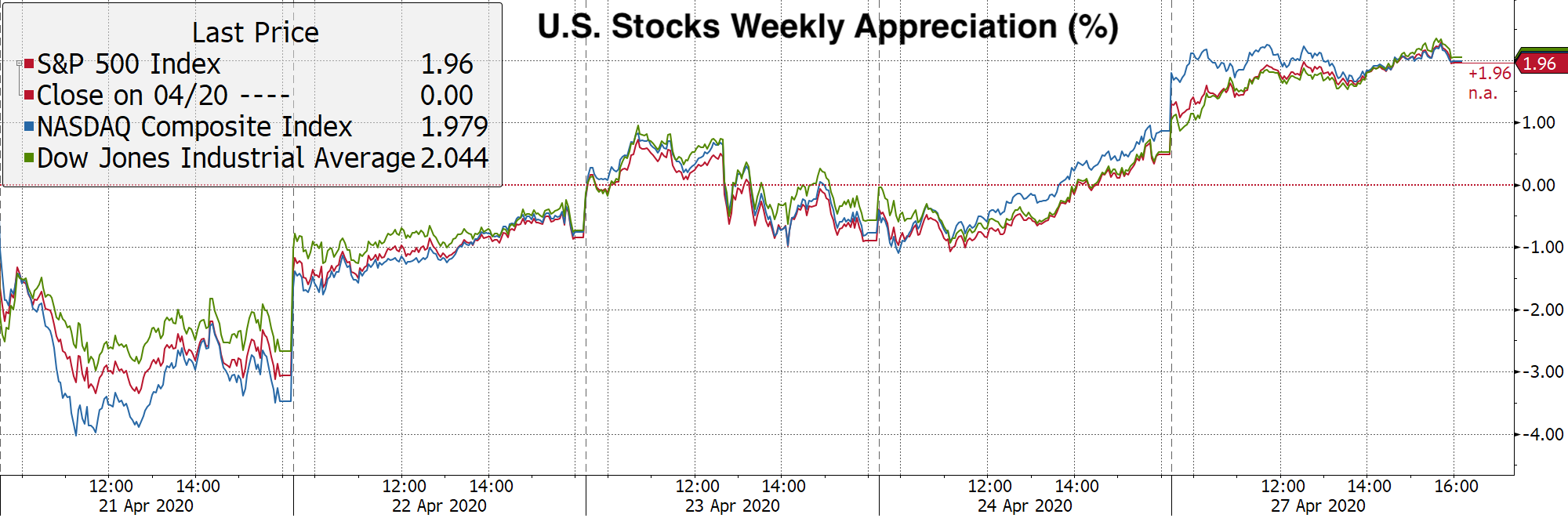

Equities performed against the backdrop of seemingly good news, as case growth decreased, several states planned to reopen their economies, and the U.S. Senate passed a new $484 billion coronavirus relief package for small businesses, $320 billion of which will go to replenish the Payroll Protection Program.

Meanwhile, the dismal economic indicators continued to trickle in through the wire. Over 4.4 million people filed jobless claims the week of April 18, bringing the five-week total up to over 26.4 million, more than all the jobs added since the Great Recession: