But back to the matter at hand. What does it all mean?

To be honest, I don’t know. I need to do more digging and see if I can find out – to see if there is a signal behind all the noise.

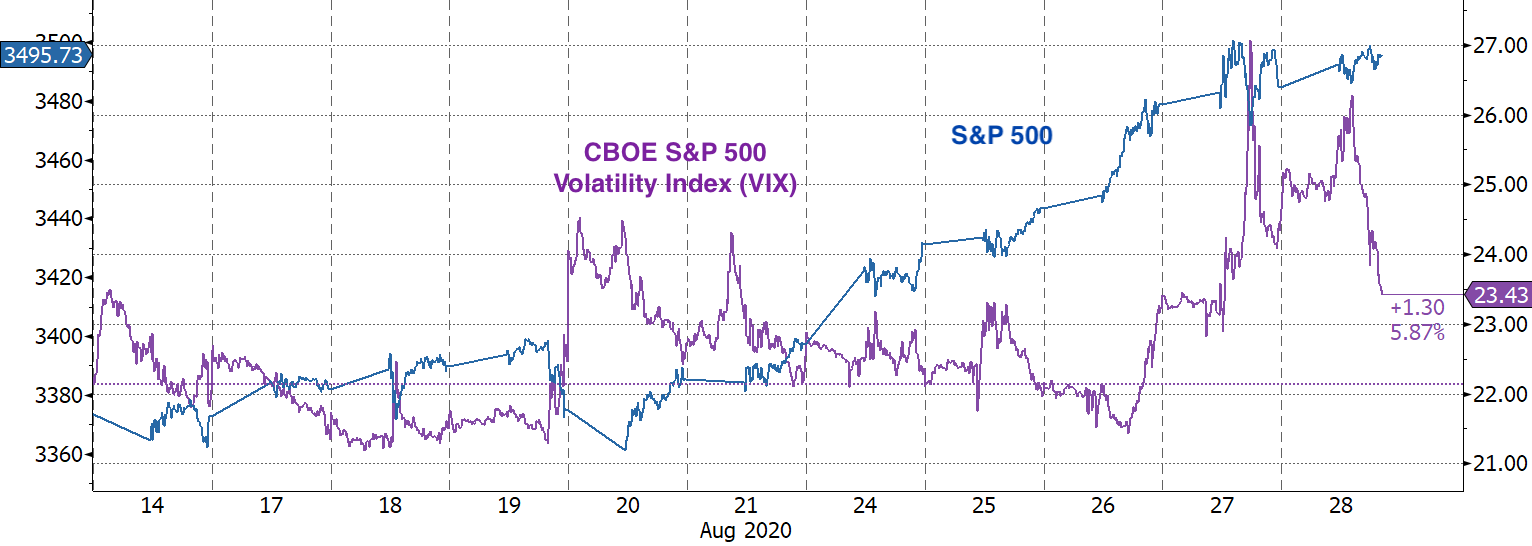

There is something Jason Buck wrote that could be a potential first breadcrumb: “you are unlikely to see this [positive] correlation in low vol environments.” So we could be in a high vol regime, and hearing the echo of this year’s “March madness”: